Online Credit Card Processing for Small Business is crucial for modern commerce. Successfully navigating the complexities of accepting online payments requires careful consideration of various factors, from choosing the right processor and setting up a secure system to understanding fees and managing potential chargebacks. This guide provides a comprehensive overview of the essential steps and considerations to help small businesses thrive in the digital marketplace.

This guide will walk you through the process of selecting a suitable credit card processor, implementing robust security measures, optimizing your payment gateway, and effectively managing fees and chargebacks. We’ll cover essential compliance regulations, strategies for minimizing costs, and tips for improving the overall customer experience during online transactions. Ultimately, our aim is to empower small businesses to confidently and profitably accept online payments.

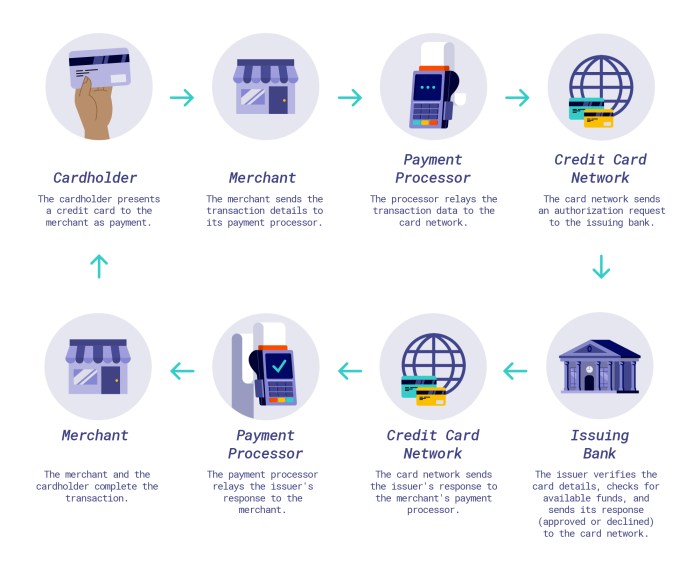

Choosing the Right Online Credit Card Processor: Online Credit Card Processing For Small Business

Selecting the appropriate online credit card processor is crucial for the financial health and operational efficiency of any small business. The wrong choice can lead to higher fees, cumbersome processes, and potential security vulnerabilities. Understanding the key features and pricing models of different providers is therefore paramount before committing to a long-term contract.

Comparison of Popular Online Credit Card Processing Services

Several popular online credit card processing services cater to small businesses, each offering a unique blend of features and pricing structures. Three prominent examples are Square, Stripe, and PayPal. Square is known for its ease of use and integrated point-of-sale (POS) system, while Stripe offers a developer-friendly API and robust customization options. PayPal, a widely recognized brand, provides a familiar interface and broad acceptance among consumers.

However, each has distinct advantages and disadvantages regarding pricing, features, and target market.

Key Factors for Selecting a Credit Card Processor

Small businesses should carefully consider several key factors when choosing a credit card processor. Transaction volume significantly impacts pricing, with higher volumes often qualifying for lower per-transaction fees. The specific industry of the business may influence the processor’s suitability, as some processors specialize in certain sectors (e.g., healthcare, e-commerce). Security features, including encryption and fraud prevention measures, are critical for protecting sensitive customer data and mitigating financial risks.

Contract terms, including early termination fees and hidden charges, should also be thoroughly reviewed before signing any agreement. Finally, customer support responsiveness and accessibility are vital factors to consider for effective problem-solving and assistance.

Comparison Table of Credit Card Processors

The following table compares the pricing models and contract terms of Square, Stripe, and PayPal for small businesses. Note that pricing can vary based on factors like transaction volume, processing type (e.g., in-person vs. online), and specific plan selected. This table provides a general overview and should not be considered exhaustive. Always refer to each provider’s official website for the most up-to-date pricing information.

| Feature | Square | Stripe | PayPal |

|---|---|---|---|

| Processing Fee (per transaction) | 2.6% + $0.10 (Visa, Mastercard) | 2.9% + $0.30 (Visa, Mastercard) | 2.9% + $0.30 (Visa, Mastercard) |

| Monthly Fee | $0 (generally) | $0 (generally) | $0 (generally) |

| Contract Terms | Month-to-month | Month-to-month | Month-to-month |

| Additional Fees | Potential for additional fees depending on features used | Potential for additional fees depending on features used | Potential for additional fees depending on features used |

Setting Up Your Online Credit Card Processing System

Successfully integrating online credit card processing is crucial for a small business’s financial health and operational efficiency. This involves choosing a processor, setting up your account, integrating with your POS system (if applicable), and implementing robust security measures. A smooth setup minimizes disruptions and ensures a positive customer experience.Setting up your online credit card processing system requires a methodical approach.

The process varies slightly depending on your chosen processor, but the fundamental steps remain consistent. Proper configuration ensures seamless transactions and minimizes the risk of errors.

Account Setup with a Chosen Processor

After selecting a credit card processor, the account setup typically involves providing business information, including your legal business name, address, tax identification number (EIN or SSN), and banking details. You’ll also need to provide information about your business’s ownership structure and the types of transactions you anticipate processing. Many processors will require verification documents, such as a copy of your driver’s license or business registration.

Following the processor’s instructions carefully is paramount. Expect to complete an application form, potentially undergo a background check, and agree to their terms of service. Once approved, you’ll receive login credentials and access to your merchant account.

Integrating with a Point-of-Sale (POS) System

Integrating your credit card processing system with your POS system streamlines operations by automating transaction recording and reconciliation. This integration typically involves downloading and installing software provided by your processor, or configuring settings within your POS system’s interface. Many modern POS systems offer direct integration options with popular processors, simplifying the setup process. If a direct integration isn’t available, you might need to use a gateway that acts as a bridge between your POS and payment processor.

The exact steps vary greatly based on your specific POS and payment processor. Thorough review of the processor’s documentation and your POS system’s instructions is crucial.

Implementing Security Measures

Protecting customer data is paramount. Failure to do so can lead to hefty fines and irreparable damage to your business reputation. Implement strong security measures from the outset. This includes using a PCI DSS compliant processor, regularly updating your software, enabling strong passwords, and employing robust firewalls. Regular security audits and employee training on data security best practices are also essential.

Consider implementing encryption for all sensitive data, both in transit and at rest. Regularly review and update your security protocols to address evolving threats. Remember, robust security isn’t a one-time task, but an ongoing commitment.

Security Checklist, Online Credit Card Processing for Small Business

Prior to launching your online credit card processing system, ensure all the following are in place:

- Chosen processor is PCI DSS compliant.

- All software is up-to-date, including the POS system and payment gateway.

- Strong passwords and multi-factor authentication are enabled.

- A robust firewall is in place and regularly updated.

- Data encryption is implemented for data both in transit and at rest.

- Regular security audits are scheduled.

- Employees have received comprehensive training on data security best practices.

Understanding Payment Processing Fees and Charges

Navigating the world of online credit card processing fees can feel like deciphering a complex code. However, understanding these charges is crucial for maintaining a healthy bottom line for your small business. This section will clarify the various fees involved and offer strategies to minimize their impact.

Online credit card processing involves several fees that directly affect your profit margins. It’s vital to understand each fee type to effectively budget and manage your expenses. Failure to do so can lead to unexpected financial strain and negatively impact your business’s overall profitability.

Transaction Fees

Transaction fees are the most common type of fee. They’re a percentage of each transaction processed, plus a small per-transaction fee. For example, a processor might charge 2.9% + $0.30 per transaction. This means that on a $100 sale, you’d pay $3.20 in transaction fees. These fees vary depending on the processor, the type of card (Visa, Mastercard, American Express, Discover), and sometimes even the type of transaction (e.g., in-person versus online).

Understanding the specific rates offered by different processors is essential for cost comparison.

Monthly Fees

Many processors charge a monthly fee for using their services, regardless of the volume of transactions processed. This fee covers the maintenance and support of the processing system. The monthly fee can range from a few dollars to several hundred dollars, depending on the features and services included in the plan. Businesses with low transaction volumes should carefully consider the balance between monthly fees and per-transaction costs.

Setup Fees

Setup fees are one-time charges incurred when you initially sign up for a credit card processing service. These fees cover the costs associated with setting up your account, providing equipment (if applicable), and training. While a one-time expense, it’s a factor to consider when comparing different processors. Some processors might waive setup fees as an incentive to attract new clients.

Chargeback Fees

Chargeback fees are incurred when a customer disputes a charge and their bank reverses the transaction. These fees can be substantial, often ranging from $15 to $50 or more per chargeback. To minimize chargebacks, focus on clear order confirmations, accurate product descriptions, and excellent customer service to prevent disputes. Implementing robust fraud prevention measures can also significantly reduce the likelihood of chargebacks.

Common Credit Card Processing Fees and Their Impact

Understanding the potential impact of each fee on your business’s bottom line is vital for effective financial planning. The following table summarizes common fees and their potential consequences:

| Fee Type | Description | Impact on Bottom Line |

|---|---|---|

| Transaction Fees | Percentage of each sale + per-transaction fee | Directly reduces profit margin on each sale; higher volume = higher total cost. |

| Monthly Fees | Recurring charge for service access | Fixed monthly expense; can significantly impact profitability for low-volume businesses. |

| Setup Fees | One-time charge for account setup | Initial investment; can be offset by long-term savings with a cost-effective processor. |

| Chargeback Fees | Fees for disputed transactions | Significant expense per chargeback; impacts profitability and increases administrative burden. |

Strategies for Minimizing Processing Fees

Negotiating lower rates with your processor is a key strategy. Processors are often willing to offer discounts to businesses with high transaction volumes or long-term contracts. Choosing a processor with transparent and competitive pricing is also crucial. Carefully compare fees and features from multiple providers before committing to a contract. Furthermore, optimizing your sales process to minimize chargebacks will significantly reduce your overall processing costs.

This includes implementing clear return policies and providing excellent customer service.

Managing Chargebacks and Disputes

Chargebacks, the reversal of a credit card transaction, represent a significant financial and operational challenge for small businesses. Understanding their causes and developing effective strategies for prevention and resolution is crucial for maintaining profitability and a positive customer relationship. This section details common causes, best practices for prevention, and the process for handling chargebacks and resolving disputes.Chargebacks arise from various reasons, often stemming from misunderstandings or discrepancies between the customer and the merchant.

Proactive measures can significantly reduce their occurrence, minimizing financial losses and preserving business reputation.

Common Causes of Chargebacks

Preventing chargebacks begins with understanding why they happen. Common causes include unauthorized transactions (where a customer disputes a purchase they didn’t make), fraudulent activity (stolen credit cards or account takeover), product or service not as described (discrepancies between advertised goods and what was received), and subscription disputes (customers forgetting about or disputing recurring charges). Addressing these issues requires a multi-pronged approach focused on clear communication, secure transactions, and robust customer service.

Best Practices for Preventing Chargebacks

Implementing effective strategies minimizes the risk of chargebacks. This includes obtaining clear authorization for all transactions, providing detailed and accurate descriptions of products or services, and having a transparent and easily accessible refund policy. Secure your website with SSL encryption to protect customer data, and actively monitor transactions for suspicious activity. Regularly review your payment processing system’s security settings and keep software updated.

Excellent customer service can resolve many potential issues before they escalate into chargebacks; promptly addressing customer inquiries and complaints can prevent dissatisfaction that might lead to a dispute.

Handling Chargebacks and Resolving Disputes

When a chargeback occurs, swift and decisive action is vital. The process typically involves receiving a notification from your payment processor, providing evidence to support the legitimacy of the transaction, and engaging with the customer to resolve the issue. This evidence might include order confirmations, shipping tracking information, and communication records with the customer. If the chargeback is deemed valid, you may need to issue a refund to the customer.

If the chargeback is deemed invalid, you can dispute it with your payment processor. Your payment processor will act as an intermediary, reviewing the evidence and making a determination.

Chargeback Dispute Process Flowchart

The following illustrates the typical steps involved in a chargeback dispute:[Diagram Description: The flowchart begins with a “Chargeback Received” box. This leads to a “Gather Evidence” box, followed by a “Contact Customer” box. These three boxes converge at a “Present Evidence to Payment Processor” box. From there, two paths emerge: one leading to a “Chargeback Won” box (with a path to “Process Refund if Necessary”), and the other leading to a “Chargeback Lost” box (with a path to “Accept Loss”).

Each box should be clearly labeled and connected with arrows indicating the flow of the process. The overall shape resembles a branching tree with the initial “Chargeback Received” as the root and the final outcomes as leaves.]

Security and Compliance for Online Payments

Protecting your business and your customers’ financial data is paramount when processing online credit card payments. Failure to prioritize security can lead to significant financial losses, reputational damage, and legal repercussions. This section Artikels key security standards and best practices to ensure compliance and safeguard sensitive information.

The Payment Card Industry Data Security Standard (PCI DSS) is the cornerstone of online payment security. Established by the major credit card brands (Visa, Mastercard, American Express, Discover, and JCB), PCI DSS is a comprehensive set of requirements designed to protect credit card information during transmission and storage. Compliance is mandatory for any business that processes, stores, or transmits credit card data.

Adherence to these standards demonstrates a commitment to data security and helps minimize the risk of data breaches and fraud.

PCI DSS Compliance Requirements

Meeting PCI DSS compliance involves several key areas. These requirements are designed to build a layered security approach, reducing the likelihood of a successful attack.

- Build and Maintain a Secure Network: This includes using firewalls, intrusion detection systems, and strong passwords to protect network infrastructure from unauthorized access.

- Protect Cardholder Data: This involves encrypting sensitive data both in transit (using HTTPS) and at rest (using encryption technologies). Data should only be stored as long as necessary and only accessible by authorized personnel.

- Maintain a Vulnerability Management Program: Regular security assessments and penetration testing identify and address vulnerabilities in systems and software before attackers can exploit them. Keeping software updated is crucial.

- Implement Strong Access Control Measures: Restrict access to sensitive data based on the principle of least privilege. This means that employees should only have access to the information they need to perform their jobs.

- Regularly Monitor and Test Networks: Ongoing monitoring of network activity helps identify suspicious behavior and potential security breaches. Regular testing ensures security measures are functioning correctly.

- Maintain an Information Security Policy: A comprehensive security policy Artikels procedures and responsibilities for handling sensitive data. All employees should be trained on this policy.

Consequences of Non-Compliance

Non-compliance with PCI DSS can result in severe penalties. These penalties can vary depending on the severity of the violation and the size of the business, but they can include:

- Fines: Significant financial penalties imposed by credit card companies.

- Increased Transaction Fees: Higher processing fees charged by payment processors as a risk mitigation measure.

- Termination of Merchant Accounts: Credit card processors may terminate the business’s ability to accept credit card payments.

- Legal Liability: Businesses may face lawsuits from customers whose data has been compromised.

- Reputational Damage: A data breach can severely damage a business’s reputation and lead to loss of customers.

Marketing and Customer Experience with Online Payments

Seamless online payment integration is crucial for boosting sales and enhancing the customer journey. A smooth and secure checkout process directly impacts customer satisfaction and encourages repeat business. This section explores strategies to optimize your online payment system for maximum impact.Integrating online payment options effectively requires a multi-faceted approach encompassing website design, marketing materials, and a focus on user experience.

Neglecting any of these areas can hinder conversion rates and damage your brand reputation.

Seamless Website Integration

Integrating online payment gateways should be straightforward and intuitive for both the business owner and the customer. Popular platforms like Shopify, WooCommerce, and Squarespace offer built-in integrations with various payment processors, simplifying the setup process significantly. For custom-built websites, developers can use APIs provided by payment processors to directly integrate payment functionality. A well-integrated system should be unobtrusive, guiding customers through the checkout process seamlessly without unnecessary distractions or confusing navigation.

For example, clear button placement and progress indicators during checkout improve user experience.

Optimizing for Mobile Devices

Given the prevalence of mobile commerce, optimizing the checkout process for mobile devices is paramount. Responsive design ensures the website adapts seamlessly to different screen sizes, preventing a frustrating experience for mobile users. Simplifying the checkout form on mobile, reducing the number of fields required, and employing intuitive design elements such as large buttons and clear visual cues are critical.

For instance, a mobile-optimized checkout might prioritize a one-click purchase option for returning customers, thereby reducing friction and improving conversion rates. A slow-loading checkout page on mobile will almost certainly lead to cart abandonment.

Effective Messaging and Design

Clear and concise messaging throughout the checkout process builds trust and encourages conversions. Using reassuring language, such as “Secure Checkout” or “Your Information is Safe,” reassures customers about the security of their transactions. Visual cues, like security badges from trusted organizations (e.g., VeriSign, McAfee Secure), further enhance security perceptions. The design should be visually appealing and consistent with your overall brand identity.

Employing high-quality images and a clean layout can significantly improve the customer experience. For example, incorporating customer testimonials or showcasing positive reviews near the checkout can build confidence and encourage purchases.

Improving Customer Experience During Checkout

Several strategies can significantly improve the online checkout experience. Offering multiple payment options (credit cards, debit cards, PayPal, Apple Pay, Google Pay) caters to a wider range of customer preferences. Providing clear and easily accessible FAQs about shipping, returns, and payment methods addresses common customer concerns. Real-time shipping cost calculations and order tracking capabilities offer transparency and build trust.

Implementing a guest checkout option allows customers to purchase without creating an account, streamlining the process for those who prefer a quicker transaction. Finally, proactive customer support, through live chat or email, addresses any immediate concerns and ensures a smooth transaction.

Choosing the Right Payment Gateway

Source: corporatetools.com

Selecting the appropriate payment gateway is crucial for the smooth operation of your small business’s online transactions. The right gateway will not only facilitate secure and efficient payments but also contribute significantly to your overall customer experience and operational efficiency. A poorly chosen gateway can lead to frustrating delays, higher processing fees, and even security vulnerabilities.Choosing the right payment gateway involves careful consideration of several key factors.

Understanding these factors and comparing different gateways will enable you to make an informed decision that best suits your business needs.

Payment Gateway Comparison: Strengths and Weaknesses

Different payment gateways offer varying features and capabilities. A thorough comparison helps identify the best fit for your specific business requirements, considering factors such as transaction volume, industry, and integration needs. Some gateways excel in international transactions, while others prioritize ease of use and integration with popular e-commerce platforms. Security features and customer support also vary significantly.

Factors to Consider When Selecting a Payment Gateway

Several key factors influence the selection of a suitable payment gateway. These factors directly impact the efficiency, security, and cost-effectiveness of your online payment processing. Careful evaluation of these aspects ensures a seamless payment experience for both your business and your customers.

- Integration Capabilities: Consider how easily the gateway integrates with your existing e-commerce platform (e.g., Shopify, WooCommerce, Magento) or point-of-sale (POS) system. Seamless integration minimizes setup time and potential errors.

- Security Features: Prioritize gateways that offer robust security features such as PCI DSS compliance, fraud prevention tools, and encryption protocols (like SSL). Strong security protects your business and your customers’ sensitive data from breaches.

- Customer Support: Reliable customer support is essential. Choose a gateway that provides readily accessible support channels (phone, email, chat) and responsive service to address any issues promptly.

- Transaction Fees: Compare transaction fees, monthly fees, and any other charges carefully. Consider the overall cost per transaction and ensure it aligns with your budget and profit margins. Hidden fees are common, so scrutinize the pricing structure thoroughly.

- Supported Payment Methods: Assess the range of payment methods supported by the gateway (credit cards, debit cards, digital wallets like PayPal, Apple Pay, Google Pay). Supporting a wider variety of payment options enhances customer convenience and potentially increases sales.

- International Transaction Capabilities: If you plan to conduct business internationally, ensure the gateway supports transactions in multiple currencies and handles international payment regulations.

Payment Gateway Feature and Pricing Comparison

The following table compares the features and pricing of three popular payment gateways. Note that pricing can vary depending on transaction volume and specific plan chosen. Always check the latest pricing information directly on the provider’s website.

| Feature | Stripe | PayPal | Square |

|---|---|---|---|

| Monthly Fee | $0 | Varies by plan, often $0 for basic | $0 |

| Transaction Fee | 2.9% + 30¢ per transaction (credit cards) | Varies by plan, typically 2.9% + 30¢ | 2.9% + 30¢ per transaction (credit cards) |

| Integration | Excellent, wide range of integrations | Excellent, wide range of integrations | Excellent, wide range of integrations |

| Security | PCI DSS compliant, robust security features | PCI DSS compliant, robust security features | PCI DSS compliant, robust security features |

| Customer Support | Generally good, multiple support channels | Generally good, multiple support channels | Generally good, multiple support channels |

Epilogue

Successfully integrating online credit card processing into your small business requires a strategic approach that balances cost-effectiveness with security and customer experience. By carefully considering the factors Artikeld in this guide—from processor selection and setup to fee management and chargeback prevention—you can establish a reliable and efficient payment system that contributes significantly to your business’s growth and profitability. Remember to regularly review your chosen services and adapt your strategies as your business evolves.

FAQ Resource

What is a payment gateway?

A payment gateway is the technology that facilitates online credit card transactions. It acts as an intermediary between your business’s website and the payment processor, securely transferring customer payment information.

How long does it take to set up online credit card processing?

Setup time varies depending on the processor and your specific needs. It can range from a few days to a few weeks. Factors like integration with existing POS systems can influence the timeline.

What are the potential legal consequences of non-compliance with PCI DSS?

Non-compliance with PCI DSS can result in hefty fines, legal action from card brands, and reputational damage, potentially impacting your ability to process credit card payments.

Can I process international transactions?

Many processors offer international transaction capabilities, but fees and processing times may vary depending on the destination country. Check with your chosen processor for specifics.

How can I reduce chargebacks?

Implement clear and concise order confirmations, provide excellent customer service, and ensure accurate product descriptions to minimize disputes and chargebacks.